For many years employer organizations, the WCB/WSIB and the Ministry of Labour claimed the Board was in financial crisis, with the myth that an “unfunded liability”* presents a danger to the viability of the workers’ compensation system, and that improvements to benefits could not be considered until it is eliminated. The Board reached a “surplus” situation by 2019, eight years earlier than its original target.

Surplus funds? The Ontario government’s 2021 Bill 27 allows the WSIB to redistribute “surplus” funds to employers. Submissions by ONIWG, IWC and other advocates protested that all cuts which reduced benefits to injured workers while eliminating the unfunded liability must first be restored in full.

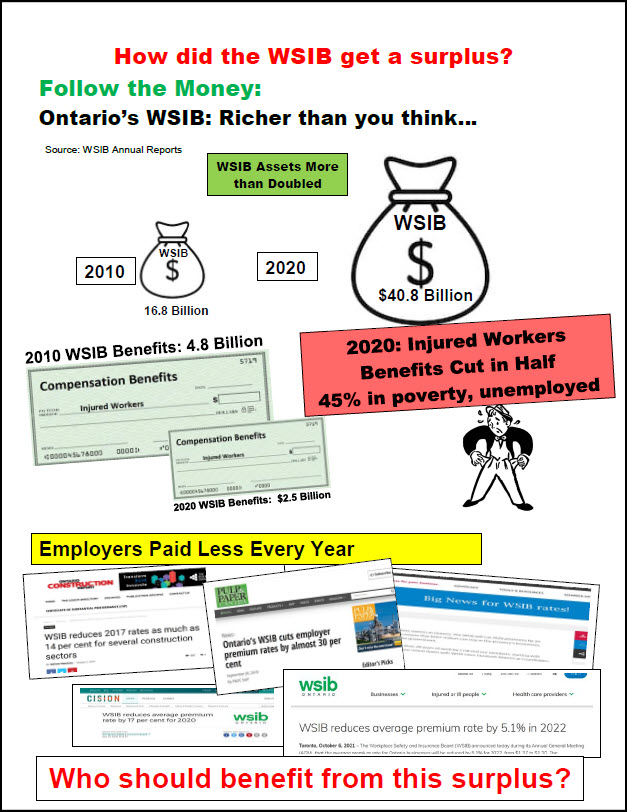

“On the backs of injured workers”

How has the current funding situation – labelled “a political slush fund” – been achieved when in 2025 employers pay lower average premium rates rates than they did 50 years ago, and their average rate has been cut by more than 50% in the last 10 years? While employers receive billions in surplus rebates and continue to see premium rate reductions, injured workers are still fighting for the restoration of benefits which were cut and pay for this surplus.

Employers’ rates kept artificially low – Employers have enjoyed generous cuts in their rates since 1996 when the average premium was $3.00 per $100 of payroll. In 2009 the WSIB produced a chart for the Chair’s consultation which shows that if employers’ assessment rates had simply been kept at that 1996 level, by the year 2006 there would have been no unfunded liability. Both the Auditor General and Harry Arthurs, chair of the Board’s 2010-2011 Funding Review, recognized that rate increases are key in covering the costs of the Board.

* What is an “unfunded liability”?

An unfunded liability is the difference between projected future costs of all the benefits of all injured workers on the books today for as long as they live and money in the bank now. The WSIB does not need to have all future payments in the bank today. As a mandatory program for employers it will always have a funding base for its future costs. As employers told Meredith, rather than a fully funded system they wanted a plan which allowed them to pay-as-you-go. That was cheaper for them than paying all the long-term costs at once.

- Grawey, Chris & Bonnie Heath. 2025 Oct. 24. The WSIB “Surplus”: A Political Slush Fund. Rankandfile.ca

- Mercer, Shane. 2025 Apr. 21. “Anger over 2nd $2B WSIB rebate.” Canadian Occupational Safety

- Ontario Network of Injured Workers Groups. 2024, Jan. 31. ONIWG-RAC Submission to Pre-Budget Hearings, Thunder Bay.

- Di Santo. Odoardo. 2014, Jun. 27. “Ontario’s Workers’ Compensation System is Under Attack.” Toronto Star

- Wilken, David K. 1998. “Manufacturing Crisis in Workers’ Compensation.” Journal of Law and Social Policy 13: 124-165.